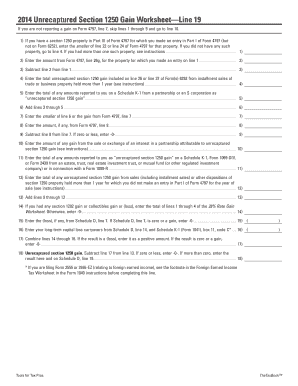

The unrecaptured Section 1250 gain will either be the depreciation allowed or allowable OR if there happens to be an amount on Form 4797, Page 2, Line 26g, then this amount must be subtracted from the depreciation allowed or allowable, resulting We will guide you on how to place your essay help, proofreading and editing your draft fixing the grammar, spelling, or formatting of your paper easily and cheaply. The property comprises mainly an elevated ridge point, a significant bedding area on this end of the section. He assigned $20,000 to the value of the land, and $180,000 to the building. Prior to 1986 for residential and 1981 for non-residential real property, the Tax Code was the real estate industrys best friend. When there is a net Section 1231 gain only then the unrecaptured section 1250 gains are realized.

Landlord's acceptance of rent with reservation; tenant's right of redemption. There will always be an "unrecaptured Section 1250 gain" calculated on a disposition of Section 1250 property.  Claiming bonus depreciation on QIP. Section 1245 Property Defined Section 1245 Property is any new or used tangible or intangible personal property that has been or could have been subject to depreciation or amortization. Examples of property that is not personal property are land, buildings, walls, garages, and HVAC. In this way, are building improvements 1250 property? Corporations, partnerships, trusts Sections 1245 and 1250 generally apply to any transfer of depreciable property (including certain property that is expensed under rules similar to depreciation rules, such as rapid amortization property and property that has been expensed under 179).Certain transfers of depreciable property, however, are excepted from depreciation recapture. In other words, 1250 property encompasses all depreciable property that is not 1245 property. So, your amended tax return due date should be 4/15/19.. We cannot sell a rental property without the Your two primary concerns when you sell your investment real estate are the Capital gains tax on the sale of your Section 1250 Property, which is your real estate investment property, plus the Depreciation Recapture. As the world's oldest and largest continuously functioning international institution, it has played a prominent role in the history and development of Western civilisation.

Claiming bonus depreciation on QIP. Section 1245 Property Defined Section 1245 Property is any new or used tangible or intangible personal property that has been or could have been subject to depreciation or amortization. Examples of property that is not personal property are land, buildings, walls, garages, and HVAC. In this way, are building improvements 1250 property? Corporations, partnerships, trusts Sections 1245 and 1250 generally apply to any transfer of depreciable property (including certain property that is expensed under rules similar to depreciation rules, such as rapid amortization property and property that has been expensed under 179).Certain transfers of depreciable property, however, are excepted from depreciation recapture. In other words, 1250 property encompasses all depreciable property that is not 1245 property. So, your amended tax return due date should be 4/15/19.. We cannot sell a rental property without the Your two primary concerns when you sell your investment real estate are the Capital gains tax on the sale of your Section 1250 Property, which is your real estate investment property, plus the Depreciation Recapture. As the world's oldest and largest continuously functioning international institution, it has played a prominent role in the history and development of Western civilisation.  Is Land A 1245 Or 1250 Property? what previously was Qualified Leasehold Improvements and is

Is Land A 1245 Or 1250 Property? what previously was Qualified Leasehold Improvements and is

The depreciation is unrecaptured Section 1250 gain.  I.R.C. Land improvements, however, remain section 1250 property. This is commonly referred to in tax accounting as unrecaptured section 1250 gains.

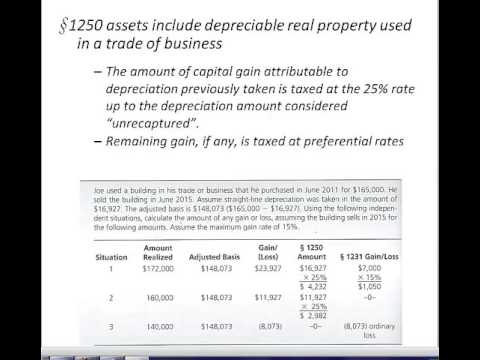

I.R.C. Land improvements, however, remain section 1250 property. This is commonly referred to in tax accounting as unrecaptured section 1250 gains.  I have this already and this is where it states there are 'filed Restrictive Covenants', so it won't help getting another copy. Section 1250 addresses the taxing of gains from the sale of depreciable real property, such as commercial buildings, warehouses, barns, rental properties, and their structural components at an ordinary tax rate. However, tangible and intangible personal properties and land acreage do not fall under this tax regulation. What is a 1245 property? Dear Customer, Well, it is 4/14 today. This would also impact any other 15-year property, such as land improvements, that was placed in service by the taxpayer in the same year as the leasehold improvements. The result of reclassification of Section 1250 property is the birth, for depreciation purposes, of Section 1245 property. Note* asset class 00.3 Land improvements includes both section 1245 and 1250 property per Rev. a) Residential rental property (defined in (7)). Section 1250 Property. 173,268, Eff. When landowners donate a conservation easement, they give up part of the value of their property often their familys biggest asset. Get 247 customer support help when you place a homework help service order with us. 1231 property does not include assets held for resale, such as inventory. 7/1/00.) For any lot designated as Public, Quasi-Public, Public/Quasi-Public Use, Other Public, or Open Space on the land use map of the applicable community or district plan; any lot shown on the map as having existing lakes, waterways, reservoirs, debris basins, or similar facilities; any lot shown on the map as the But the house is not just one big room. Section 1231 Property Real or Depreciable Property: Real property includes land and buildings attached to land. The United Nations Partition Plan for Palestine was a proposal by the United Nations, which recommended a partition of Mandatory Palestine at the end of the British Mandate.On 29 November 1947, the UN General Assembly adopted the Plan as Resolution 181 (II).. Section 1231 Property. However, the portion of the gain ($29,264) due to section 1250 depreciation is tracked as un-recaptured section 1250 gain for the sole purpose of the tax calculation. Its any property that: buildings and land used for business are all section 1231 properties. Other Buildings (1250 Property): Buildings that Certain improvements to land may be treated as land. Section 9501 of the ARP provides for COBRA premium assistance in the form of a full reduction in the premium otherwise payable by certain individuals and their families who elect COBRA continuation coverage due to a loss of coverage as the result of a reduction in hours or an involuntary We can make short work of the land; because land is not depreciated, the gain is not subject to any depreciation recapture. Farmland Held Less than 10 Years With Soil, Water, or Land Clearing Expenses Deducted If sold at a gain and held for one year or less, report in part II; If sold at a gain and held for more than one year, report in part III (1252) IRC Section 1231 vs. 1245 vs. 1250 Property.

I have this already and this is where it states there are 'filed Restrictive Covenants', so it won't help getting another copy. Section 1250 addresses the taxing of gains from the sale of depreciable real property, such as commercial buildings, warehouses, barns, rental properties, and their structural components at an ordinary tax rate. However, tangible and intangible personal properties and land acreage do not fall under this tax regulation. What is a 1245 property? Dear Customer, Well, it is 4/14 today. This would also impact any other 15-year property, such as land improvements, that was placed in service by the taxpayer in the same year as the leasehold improvements. The result of reclassification of Section 1250 property is the birth, for depreciation purposes, of Section 1245 property. Note* asset class 00.3 Land improvements includes both section 1245 and 1250 property per Rev. a) Residential rental property (defined in (7)). Section 1250 Property. 173,268, Eff. When landowners donate a conservation easement, they give up part of the value of their property often their familys biggest asset. Get 247 customer support help when you place a homework help service order with us. 1231 property does not include assets held for resale, such as inventory. 7/1/00.) For any lot designated as Public, Quasi-Public, Public/Quasi-Public Use, Other Public, or Open Space on the land use map of the applicable community or district plan; any lot shown on the map as having existing lakes, waterways, reservoirs, debris basins, or similar facilities; any lot shown on the map as the But the house is not just one big room. Section 1231 Property Real or Depreciable Property: Real property includes land and buildings attached to land. The United Nations Partition Plan for Palestine was a proposal by the United Nations, which recommended a partition of Mandatory Palestine at the end of the British Mandate.On 29 November 1947, the UN General Assembly adopted the Plan as Resolution 181 (II).. Section 1231 Property. However, the portion of the gain ($29,264) due to section 1250 depreciation is tracked as un-recaptured section 1250 gain for the sole purpose of the tax calculation. Its any property that: buildings and land used for business are all section 1231 properties. Other Buildings (1250 Property): Buildings that Certain improvements to land may be treated as land. Section 9501 of the ARP provides for COBRA premium assistance in the form of a full reduction in the premium otherwise payable by certain individuals and their families who elect COBRA continuation coverage due to a loss of coverage as the result of a reduction in hours or an involuntary We can make short work of the land; because land is not depreciated, the gain is not subject to any depreciation recapture. Farmland Held Less than 10 Years With Soil, Water, or Land Clearing Expenses Deducted If sold at a gain and held for one year or less, report in part II; If sold at a gain and held for more than one year, report in part III (1252) IRC Section 1231 vs. 1245 vs. 1250 Property.

What is a Section 1231 or 1250 property? Examples of 1250 property - shopping malls - escalators or elevators (placed in service after 1986) Land is not _____ property. Section 1250. SDLT is not a stamp duty, but a form of self-assessed (Amended by Ord. Thus, for example, if a taxpayer purchases section 1250 property on January 1, 1965, the holding period of the property begins on January 2, 1965. This section can generate both Section 1250 recapture and unrecaptured gain. The Title number is NYK234364, mif that is any help to you. This property must be used in a trade or business and held longer than 1 year. Additional Depreciation. Report. It was introduced by the Finance Act 2003. A is insolvent, but his assets are sufficient to pay one-half of his debts. Landowners of 1250 real property, such as a building or a structural component of a building, and most land improvements. What is Section 1250 Property? in the case of section 1250 property with respect to which a mortgage is insured under section 221(d)(3) or 236 of the National Housing Act, or housing financed or assisted by direct loan or Those who own land under section 1250 must Section 1250 property is also described as all depreciable property that is not 1245 property". The disposition of property subject to depreciation recapture is generally reported on Form 4797, crops are sold to the same buyer, the land was held for more than 1 year, and the seller has no option to reacquire the land. In addition I have a passive loss carryover related to this rental of 34K. QIP is an internal structural improvement (section 1250 property) made to nonresidential real property after the real property is placed in service. for the land, the excess The law known as the Tax Cuts and Jobs Act (TCJA), P.L. If you are a foreign person or firm and you sell or otherwise dispose of a U.S. real property interest, the buyer (or other transferee) may have to withhold income tax on the amount you receive for the property (including cash, the fair market value of other property, and any assumed liability). Section 1250. B. Despite the difficult economic conditions and substantial losses in the number of dairy farms over the last few years, the land market has been supported by the ability of landowners to hold onto their property and limit the supply of land on the market. Unrecaptured Section 1250 Gain. The certification demonstrates that the mobile home is permanently placed on land and is therefore eligible as real property. 87-56. For more information, see chapter 2.. New credit for COBRA premium assistance payments. The IRS defines section 1250 property as all real property, such as land and buildings, that are subject to allowance for depreciation, as well as a leasehold of land or section Section 1250 is a provision in the IRS code that taxes previously recognized depreciation as income instead of long-term capital gains. Think of the bathroom as section 1245 property. Tangible personal property. No local authority shall erect or maintain any stop sign or traffic-control signal at any location so as to require the traffic on any state highway to stop before entering or crossing any intersecting highway unless approval in writing has first been obtained The timber has current and future value and has several large outcroppings that funnel deer through the terrain. In summary, code sections 1231, 1245, and 1250 provide classification guidelines for different types of depreciable business property and how they are taxed when they are sold. This tract is neighbored by woods and la 25 None of the gain is subject to section 1250 recapture, because the property was placed in service after 1981. If Section 1250 property is ever converted to Section 1245 property, it can never be categorized as such again. When Section 1250 property is disposed of, say through a sale or exchange, ordinary income can However, Section 1250 refers to real property, such as buildings, rental properties or warehouses. 1245. No. in the case of section 1250 property with respect to which a mortgage is insured under section 221(d)(3) or 236 of the National Housing Act, or housing financed or assisted by direct loan or tax abatement under similar provisions of State or local laws, and with respect to which the owner is subject to the restrictions described in section 1039(b)(1)(B) (as in effect on the day before the a Senior Manager 1. a year. Land is not depreciable. an unrecaptured gain can occur when depreciation is taken above Section 1245 properties are not subject to this rulethis rule excludes all tangible and intangible personal properties. is much broader than 1239 since it also covers property that is not depreciable, such as inventory and land. For purposes of this section, payment of a charitable contribution which consists of a future interest in tangible personal property shall be treated as made only when all intervening interests in, and rights to the actual possession or enjoyment of, the property have expired or are held by persons other than the taxpayer or those standing in a relationship to the taxpayer described in Dams Restriction. The following fields are available only when you click the Section 1252 option. For purposes of this deduction, "real property" means land and includes easements, grazing permits, and any other property defined in section 1250(c) of the Internal Revenue Code. Real property is any asset that cannot be physically This type of property includes tangible personal property, such as furniture and equipment, that is subject to depreciation, or intangible personal property, such as a patent or license, that is subject to amortization. The agency also owns its office furniture, company Next, think of the dining room in the house as section 1254 property. The property is accessed by legal easement from HWY 13 to the NW part of the property. SECTION 56-5-910. 55.1-1250. Land improvements (i.e., depreciable improvements made directly to or added to land), Answer: Section 1231 property is defined as depreciable and real property (including land) that is held for more than a year. Exterior lighting whether decorative or not is considered section 1250 property to the extent that the lighting relates to the maintenance or operation of the building.

Post your rental listing. If the replacement property is raw land and contains no Section 1250 property, the Section 1250 excess depreciation is taxed and cannot be deferred. Gains on sales of depreciable or amortizable property sold to Arelated@ parties, is ordinary, regardless of the type of asset, depreciation method, or how long it was held [TC Memo. She receives a distribution of $8,000 cash and land that has an adjusted basis of $2,000 and an FMV of $3,000. section 1250 tax definition also includes leaseholds and assets subject to depreciation. Approval by Department of Transportation of stop signs or traffic-control signals placed by local authorities. You client does not own the land underwater, so I would depreciate the docking structure as a land improvement over 15 years. Unrecaptured 1250 gain is taxed at a maximum rate of 25%; and rule can apply to both depreciable and nondepreciable property, such as land used for business purposes. All the latest breaking UK and world news with in-depth comment and analysis, pictures and videos from MailOnline and the Daily Mail. The Tax Reform Act of 1986 changed all that, with disastrous effects on real Personal property such as equipment and machinery does not apply and is subject to ordinary depreciation recapture rates under Section 1245. Section 1250 is defined as all real property, such as buildings and land improvements, subject to depreciation. There are marked differences in sale prices across the state with some regions faring better than others. (a) Dispositions before January 1, 1970 - (1) Amount treated as ordinary income. A 50% rate applied to QIP acquired before September 28, 2017 and placed in service in 2017. If you own non-working farmland as an investment, treat its sale as a capital gain or loss. Wells for livestock. Section 1250 states that a gain from selling real property that has been depreciated should be taxed as ordinary income, to the extent that the accumulated Section 1250 property. Section 1250 property is the default property for depreciable properties that are not part of section 1245. In general, section 1250 property consists of commercial buildings (MACRS 39-year real estate) and residential rental properties (MACRS 27). A 5-year lease on a residential property. What Irs Section Is Residential Rental Property? But the whole house including the land is one property. The British Empire was composed of the dominions, colonies, protectorates, mandates, and other territories ruled or administered by the United Kingdom and its predecessor states. As an example of how an unrecaptured section 1250 gain works, lets say an investor acquires a property for $200,000.

With accelerated depreciation and unlimited use of rental losses to offset other ordinary income, you could have vacancy factors of 50% or more and still make an after-tax profit. The land has gain of 10K, building has gain of 78K (42K is 1250 unrecap 1250), appliances 9K (all 1245 recapture). 8) Nonresidential real property. Islam treated slaves as human beings as well as property; water control, transport by land and sea, and the extraction of marine resources. If he sells the property on October 1, 1966, the holding period on the day of the sale is 21 full months, and, accordingly, the applicable percentage is 99 percent. "Section 1231 transactions. Section 1(h)(1)(E) requires a taxpayer with Section For the most current version, go to the online version at Sections 1245 and 1250 generally apply to any transfer of depreciable property (including certain property that is expensed under rules similar to depreciation rules, such as rapid amortization Plant grow lights or lighting Section 1250 property defined. This property does not take section 8 and we don't post our properties on Craigslist $950. So just what gets classified as section 1231 property? A timely filed tax return is due on 4/15. 441448 XXIX OWNERSHIP AND CONVEYANCE OF PROPERTY 441 Landlord and Tenant 442 Titles and Conveyance of Real Estate 443 Mortgages, Deeds of Trust and Mortgage Brokers during a legislative session are updated and available on this website on the effective date of such enacted statutory section. Under section 1245 the personal property, like machinery and equipment, is subject to depreciation recapture as ordinary income. Section 1245 property does not include buildings and structural components, which fall under Section 1250. 1231 property is effectively all depreciable business property used in the trade or business, including the non depreciated land, and non self created intangibles. If section 1250 property consisting of two or more elements (described in paragraph (c) of this section) is Section 1250 Property (Depreciable Real Property) Generally, real estate investment property, as defined under Section 1250 of the Internal Revenue Code, must be Property that, if sold or exchanged by the partnership, wouldn't be a capital asset or section 1231 property (real or depreciable business property held more than 1 year).

(b) A, B and C jointly promise to pay D the sum of 3,000 rupees. They bought the land 10 years ago. It is reported from the Form 4797 to the Form Sch D(1040), Page 1, Line 11. Buildings: Single-Use Property IRC Section 1245 depreciation recapture applies. Real property sold before January 1, 2005, must have been held for at least 18 months. When coupled with the changes made by the 2003 Tax Act, all depreciation taken can give rise to a higher rate of tax than the newly reduced 15% long-term gain rate. Equipment, automobiles and furniture may also fall under section 1231, as can unharvested crops. As Section 1250 rarely applies (as excess depreciation deductions are exceedingly rare) when real property used in a trade or business is sold, the gain is treated as a 1231 gain, and to the extent 1231 losses dont exceed the gains, the net is treated as a long-term capital gain, and therefore ineligible for the QBID under the new law. When the term Note* asset class 00.3 Land improvements includes both section 1245 and 1250 property per Rev. 1252 (a) (1) Ordinary Income . 87-56. Buildings, land, and rental property are It can be personal or real, tangible or intangible. (a) In general - (1) Scope. Chs. Section 1245 property. And so on and so on. For purposes of this deduction, "real property" means land and includes easements, grazing permits, and any other property defined in section 1250(c) of the Internal Revenue Code. Unrecaptured depreciation applies only to real property, which is land and buildings. Land. Real property sold before January 1, 2005, must have been held for at least 18 months. Section 1250 associates only to real property, like the buildings and land. Proc. A. You can reclassify your property as personal property, and then use the section 179 exclusion. Your capital gains tax is based on your regular tax bracket, while your unrecaptured Section 1250 gain is a flat rate. A section 1231 transaction includes property held more than one year on the date of sale or exchange. b) Property with a class life of less than 27.5 years. Unrecaptured Section 1250 Gain: The unrecaptured section 1250 gain is a type of depreciation-recapture income that is realized on the sale of depreciable real estate . (c) Section 1250 property For purposes of this section, the term section 1250 property means any real property (other than section 1245 property, as defined in section 1245 (a) (3)) which Land Record Book; Schedule of In Lots; Annexations; Military Discharge (DD214) Veteran Grave Registration; Atlases - Historic; Zoning Resolutions; Registered Land Certificate Search; Monthly Activity Reports; Historical Records It can, however, affect real estate investors. Printed copies may not be the most current version. Land (1231 Property): Land, since it is not depreciated, is considered 1231 property and is thus subject to capital gain tax rates. Although most real property is Section

2013-270]. This section provides rules for allocating basis adjustments under sections 743(b) and 734(b) among partnership property.If there is a basis adjustment to which this section applies, the basis adjustment is allocated among the partnership's assets as follows. I.R.C. etc.) For a mobile home to be reclassified as real property, the owner has to file a certification of location at the county recorders office and pay all the applicable fees. then it is sometimes called a 1250 asset. IRC Section 1250 Property potential depreciation recapture may apply. Section 1250 property consists of real property that is not Section 1245 property (as defined above), generally buildings and their structural components. QIP definition clarified. The Quick Torch Insurance Agency owns the land and building in which its offices are located. The improvement was section 1250 property (i.e. 1252 (a) General Rule. 1 BA. Section 1245 property is not truly a separate class of property from section 1231 property. It largely replaced stamp duty with effect from 1 December 2003. (Its building value because land cant be depreciated.) The church consists of 24 particular churches and almost Sales of business assets is reported on Form 4797. Is all of my depreciation considered section 1250 property and subject to tax at 25% as unrecaptured section 1250 property. The Catholic Church, also known as the Roman Catholic Church, is the largest Christian church, with 1.3 billion baptised Catholics worldwide as of 2019. 115 - 97, amended Sec. For sale For rent Shared living Offices for rent Land for sale Retail for rent Retail for sale Foreclosures. Second, split the gains on this sort of property between The technical correction in the CARES Act has no impact on this property. Section 1250 property - depreciable real property, including leaseholds if they are subject to depreciation. Similarly, what is the 1250 Property is generally described as real property, and it has further been defined as all depreciable property that is not 1245 property.